2023: Year of continued wariness

21 March 2023

As we move towards the second quarter of 2023, it is clear that the remainder of this year will most likely be characterized by wariness, in continuation of last year’s high levels of economic uncertainty. Over the course of 2022, uncertainty reigned as global economic growth was weighed down significantly by rapid increases in living expenses, owing largely to commodity shortages resulting from the escalation of the war in Ukraine, and the lingering COVID pandemic.

In an effort to fight inflationary pressures, many central banks tightened their monetary stance during 2022. However, the surge in interest rates led to deteriorated financial market conditions, exacerbating the existing economic uncertainty. So far this year, the battle to tame inflation continues with no clear end in sight, triggering fears that a global recession is imminent. The failures of several banks early in March 2023 added to the existing wariness about economic and financial developments in the coming period.

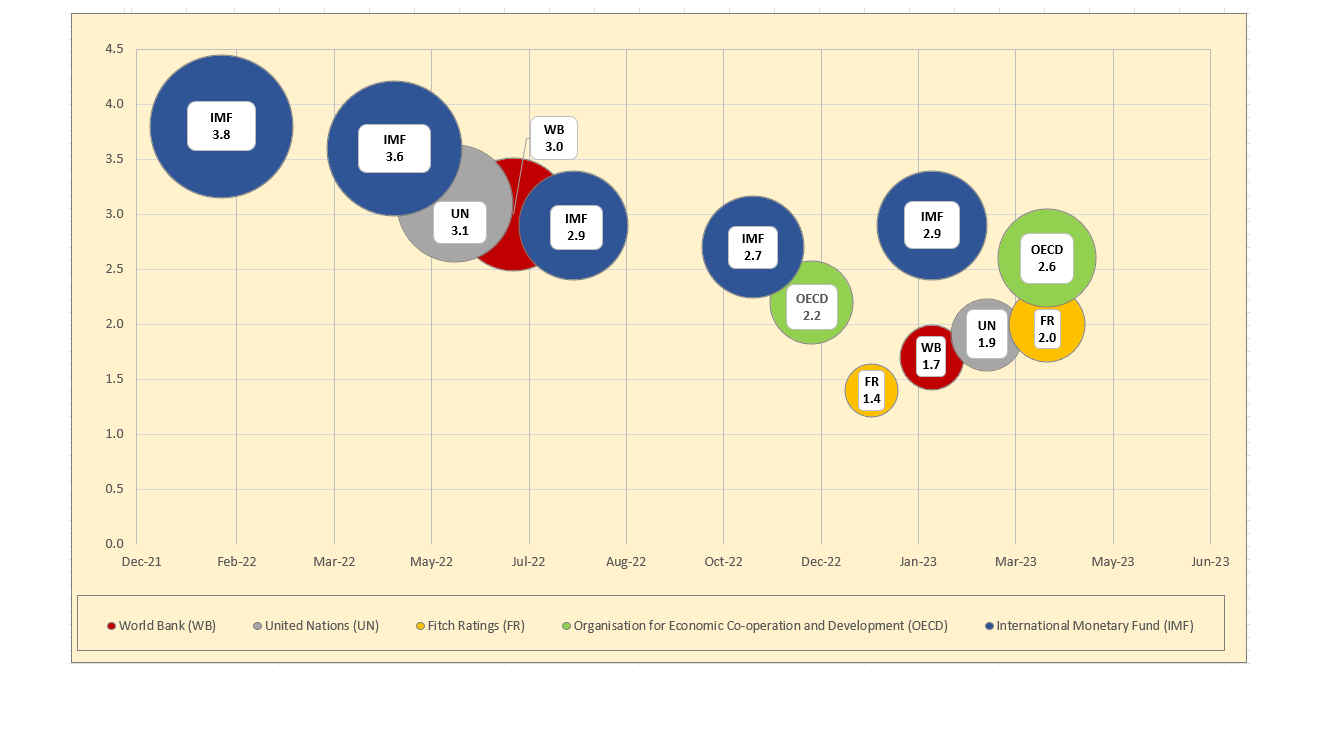

So far, several projections have been issued of real Gross Domestic Product (GDP) in 2023, for the world economy as a whole, as well as for individual countries and different country groups. A review of a selection of global growth projections made for 2023 reveals that Fitch Ratings’ forecast of 1.4% [December 2022] was the lowest, while the International Monetary Fund (IMF)’s 2.9% [January 2023] is the highest to date. (See Table I for an overview.)

Table I – Selected global growth projections for 2023 ( % , release month)

The World Bank’s global growth prediction of 1.7% [January 2023], was remarkably lower than that of the IMF. Moreover, the World Bank’s forecast entailed a relatively sharp downward adjustment compared to its own earlier forecast, namely 3% [June 2022]. This downward adjustment was led by a lowering of the World Bank’s growth expectations for a vast majority of the countries in the world. According to the World Bank, even a small shock could push the global economy over the edge, into a recession. Possible shocks include higher-than-anticipated inflation, sudden interest rate hikes to tame inflation, escalating geopolitical conflicts, or a resurgence of the COVID-19 pandemic. The United Nations (UN)’s forecast of 1.9% [February 2023], and its underlying assumptions are fairly in line with those of the World Bank. The UN expressed concern that many developed and developing nations face risks of recession in 2023.

Contrastingly, the IMF stated in its January 2023 World Economic Outlook report (WEO) that a global recession is not included in its baseline. This decision was based, among other things, on the European economies having so far weathered the energy crisis better than anticipated. The reopening of China’s economy in December 2022 is also expected to have a positive impact on global output in 2023, according to the IMF. Similar considerations led both Fitch Ratings and the Organisation for Economic Co-operation and Development (OECD) to recently raise their global growth expectations for 2023, to respectively, 2% [March 2023 ] and 2.6% [March 2023]. Notwithstanding its upward growth revision, Fitch Ratings expects that several major developed markets will experience recessions during 2023.

Figure I – Selected Growth projections for 2023

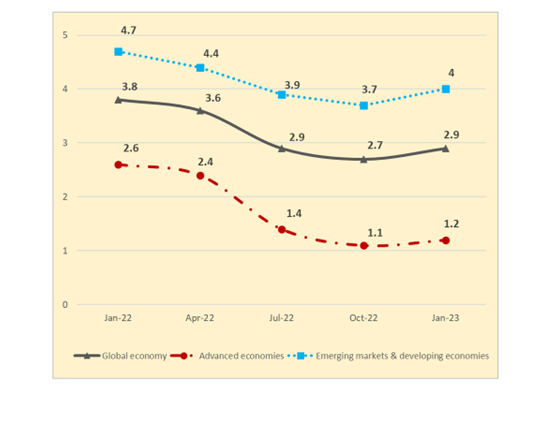

A review of the IMF’s growth projections for 2023 issued in the January 2022-October 2022 period, reveals that its most recent forecast of 2.9% might seem somewhat positive compared to those of other institutions, but that it is lower than most of the IMF’s earlier quarterly forecasts for the year 2023. According to the IMF, its latest projection is lower than the historical average global growth of 3.8 % registered in the period 2000-2019. The IMF foresees that the below-trend expansion of global output during 2023 will be driven by lower growth not only in the advanced economies, but also in the emerging markets & developing countries. (See Figure I and Figure II.)

Figure II – The IMF’s growth projections for 2023 (release period January 2022-January 2023)

In the coming several weeks, more information will become available about 2023’s first-quarter developments in worldwide economic output levels, inflation levels, financial market developments, labor market conditions, and other key economic indicators. One of the crucial determinants of overall global economic performance in the coming months is how well central banks will be able to subdue inflationary pressures while preventing further turmoil in financial systems worldwide. The Black Sea Grain Initiative, which enables the export of food and fertilizers from Ukraine, is also a key determinant of global food prices and nutrition security in the short run. On March 18, 2023, this Initiative was renewed for a minimum of 60 days, but after seemingly tense renegotiations between warring Russia and Ukraine. When negotiations have to restart again, this could result in renewed concerns about nutrition security, and new waves of food prices hikes due to scarcity. Barring a resolution to the war in Ukraine in 2023, energy prices might also become a bigger challenge if a rough winter period is expected in the northern hemisphere. Concluding, as these various developments continue to unfold during 2023, the existing wariness about economic and financial developments around the world will continue to linger.

Sources:

- Fitch Ratings — Global Economic Outlook – December 2022, & March 2023.

- International Monetary Fund — World Economic Outlook – January 2022, April 2022, July 2022, October 2022, & January 2023.

- Organisation for Economic Co-operation and Development – OECD Economic Outlook – November 2022, & Interim Report March 2023.

- United Nations — World Economic Situation and Prospects 2023 – January 2023.

- World Bank — Global Economic Prospects – June 2022 & January 2023.

- Reuters — Davos 2023: Key takeaways from the World Economic Forum – January 20, 2023; Ukraine Black Sea grain deal extended for at least 60 days – March 18, 2023.